FolioBeyond Fixed Income Commentary For February 2020

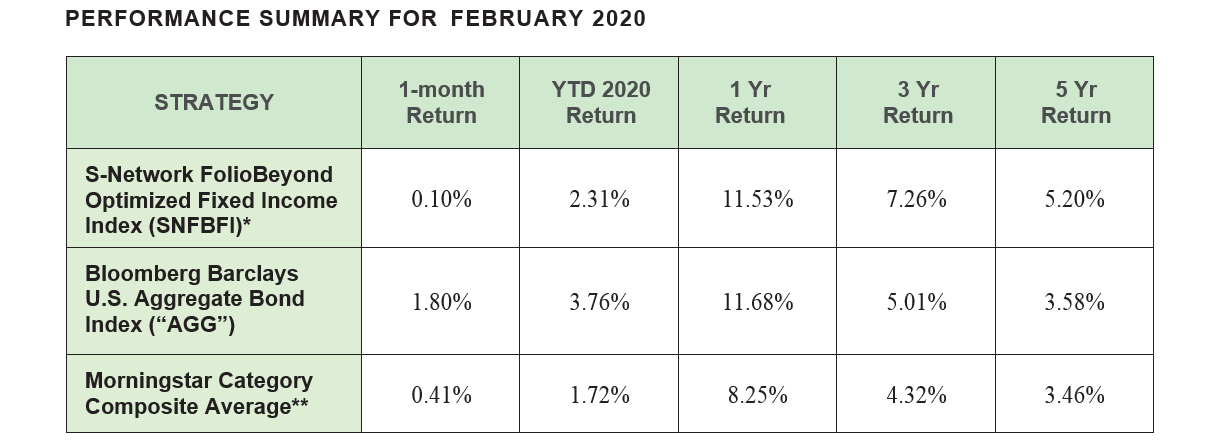

FolioBeyond’s algorithm underlying the S-Network FolioBeyond Optimized Fixed Income Index (SNFBFI) was up 0.10% in February versus 1.80% for the Bloomberg Barclays U.S. Aggregate Bond Index (“AGG”). Over the past 12 months, SNFBFI has generated comparable returns as AGG while it has outperformed during the past three- and five-year periods.

The flight to quality rally accelerated in February as the 10-year Treasury yield declined by 38 basis points to reach a historic month-end low of 1.13%. The 2-year Treasury followed suit with a 47 bp drop to end the month at 0.86% yield. Credit sectors lagged the rally and continued to cheapen as the uncertainty around Coronavirus persisted. Implied volatility levels in the 1-year swaption market spiked to around 170% of historicals.

* SNFBFI’s returns are net of underlying ETF fees and 30 bp assumed management fee. Although the information herein is believed to be reliable, FolioBeyond makes no representation or warranty as to its accuracy, and information and opinions reflected herein are subject to change at any time without notice. The past performance information presented herein is not a guarantee of future results.

** Composite figures are simple averages and include actively managed mutual funds from Morningstar Categories US Intermediate Core-Plus Bond, US Fund Multisector Bond, and US Fund Nontraditional Bond.

This type of rapid dislocation has generated more rebalancing trades as the model breached risk thresholds multiple times during the month. While there were a few minor portfolio changes over the course of the month, the major shifts consisted of a reduction of Mortgage REIT exposure replaced by Agency MBS and Bank Loan exposures. Intra-month, the model also increased exposure to long duration Treasuries. The major factors that drove portfolio adjustments were spikes in implied volatility, ongoing changes in relative value relationships and strong momentum effects.

In order to quantify the “alpha” generated by an algorithmic rebalancing of the model, we compared the actual performance of SNFBFI to a static portfolio set to beginning-of-month allocations. The main takeaway from this comparison was that the model outperformed the static portfolio by 227 basis points, mainly from the de-risking of Mortgage REIT exposure and the intra-month increase of long duration Treasuries.

As we have seen in past downturns, our dynamic model should be able to recapture short-term underperformance versus the benchmark in subsequent months after the downward momentum effects subside and the relative value component becomes more attractive. Given the current environment, the rapidly changing dynamics of the market make it even more compelling to utilize a robust, algorithmic approach for capturing multiple Fixed Income risk and value factors within an optimization framework where current market levels and analytical measures are constantly updated on a daily basis. Furthermore, this ultra-low interest rate environment we are now in will make a dynamic, systematic approach more compelling for extracting sector allocation alpha and generating attractive risk-adjusted returns over intermediate and long-term holding periods.

Please contact us to explore how our low-cost, efficiently executed algorithmic strategy can fit into your Fixed Income bucket, or how the model can be customized to suit your specific investment needs.