FolioBeyond Fixed Income Commentary For March 2020

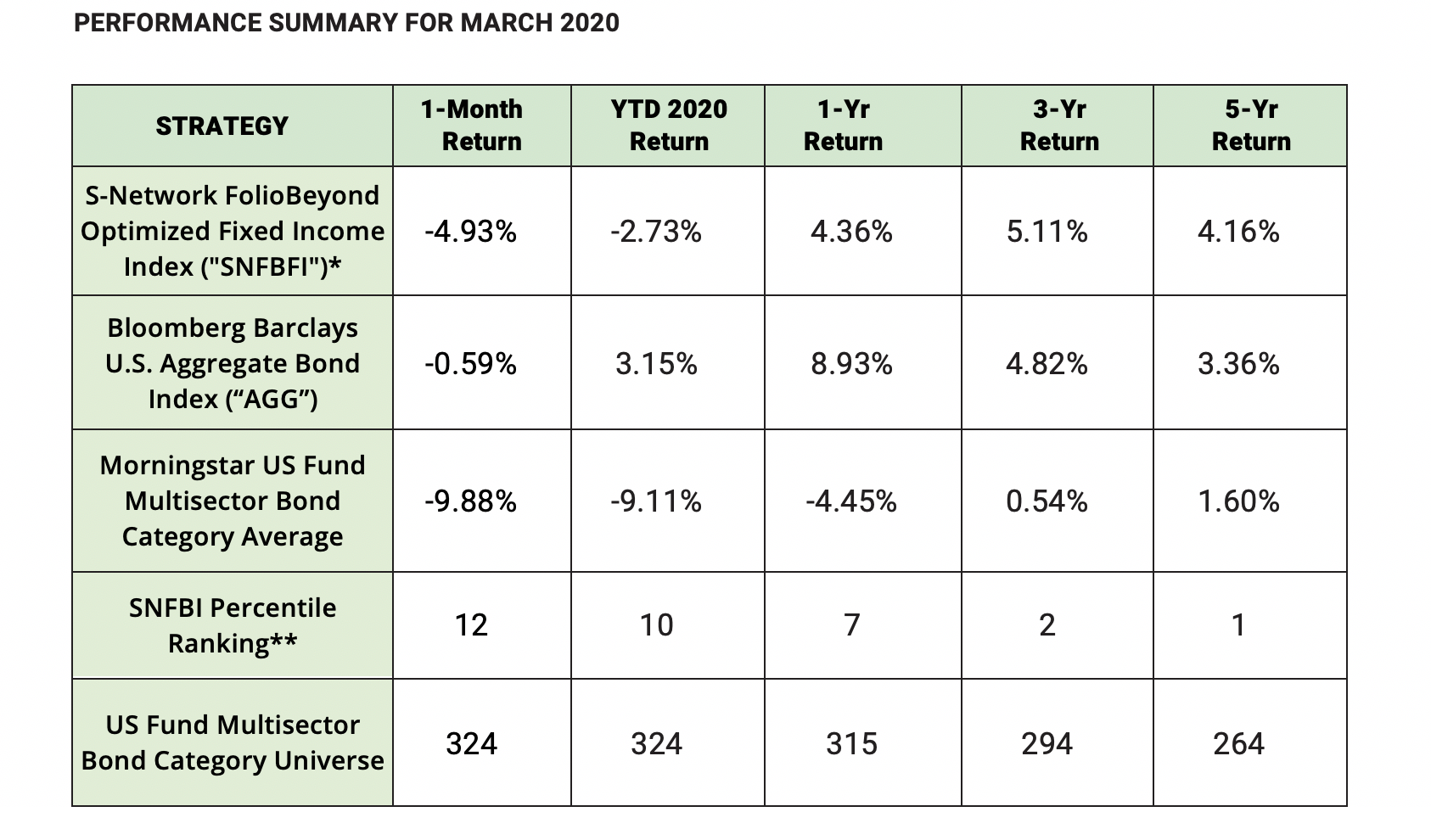

FolioBeyond’s algorithm underlying the S-Network FolioBeyond Optimized Fixed Income Index ("SNFBFI") returned -4.93% (net of 30bp fee assumption) in March versus -0.59% for the Bloomberg Barclays U.S. Aggregate Bond Index (“AGG”). However, SNFBFI performed well in comparison to its peer group (Morningstar’s US Fund Multisector Bond category) beating the category average by just under 5%. Over longer time periods SNFBFI continues to outperform both benchmarks as shown below for 3 and 5-year holding periods.

The primary factors that drove the divergence of performance during this month's historic volatility is a tale of portfolio duration and sector rebalancing. AGG by its nature has a heavy proportion of US Treasuries and Agencies, including Mortgage Backed Securities ("MBS"), and Investment Grade bond exposure. AGG benefitted from the dramatic flight-to-quality rally in US Treasuries, further supported by the Fed’s unprecedented effort to stabilize the MBS market.

In terms of sector rotation, the unparalleled speed at which the Coronavirus pandemic permeated the economy caught markets off guard, leaving Multisector bond managers with little time to react. This was compounded by limited liquidity in the secondary market for trading large cash bond portfolios.

Source: Morningstar

* SNFBFI’s returns are net of underlying ETF fees and 30 bp assumed management fee. Although the information herein is believed to be reliable, FolioBeyond makes no representation or warranty as to its accuracy, and information and opinions reflected herein are subject to change at any time without notice. The past performance information presented herein is not a guarantee of future results.

** The Rank is calculated using the total return of the S-Network FolioBeyond Optimized Fixed Income Index ("SNFBFI"), ranked against the closing total returns of the open-end mutual funds in Morningstar's US Fund Multisector Bond Category. Percentile Rank is the total-return percentile rank of SBFBFI relative to all funds in the defined Morningstar Category. The highest (or most favorable) percentile rank is 1 and the lowest (or least favorable) percentile rank is 100.

FolioBeyond’s strategy outperformed Morningstar’s Multisector Bond category by algorithmically rebalancing, as needed, to daily changes in relative value relationships, implied volatility levels, momentum effects and other factors that drive the daily optimization process. A traditional approach to asset management would have likely been challenged to programmatically readjust the portfolio as market conditions changed significantly on a daily basis.

FolioBeyond’s model ETF portfolio started the month with a mix of long duration US Treasuries, Agency MBS, short-dated High Yield Corporates, Bank Loans, and High Yield Municipal Credit. However, as risk levels spiked to historic highs, the ETF portfolio was quickly rebalanced in the first week of the month shifting exposure to short-duration High-Grade sectors including US Treasuries, Municipals, Corporates, and Treasury Inflation-Protected Securities ("TIPs"), combined with significant exposure to intermediate duration US Agency bonds. As of month-end, the portfolio primarily consisted of US Agency bonds, short-duration US Treasuries and TIPs, along with a small allocation to short duration High Yield Corporates.

To demonstrate the asset allocation alpha generated by our model, the table below compares the performance of the strategy versus a static portfolio set to year-end 2019 model allocations. If the portfolio was maintained at the 2019 year-end allocations without any rebalancing, the resulting performance would have been worse by 18.21% year-to-date This differential highlights the importance of optimized risk-based rebalancing, especially in times of unexpected market volatility.

Source: Morningstar

* SNFBFI’s returns are net of underlying ETF fees and 30 bp assumed management fee. Although information herein is believed to be reliable, FolioBeyond makes no representation or warranty as to its accuracy, and information and opinions reflected herein are subject to change at any time without notice. The past performance information presented herein is not a guarantee of future results.

** Total Return of 12/31/19 Allocations is the year-to-date weighted average total return of the S-Network FolioBeyond Optimized Fixed Income Index ("SNFBFI") portfolio allocations ("Allocations") as of 12/31/19. Allocations as of 12/31/19 were, by ticker, TLT 8.956%, SJNK 30.004%, HYG 1.033%, HYD 30.003% and REM 30.004%. The source for portfolio total return values is Morningstar.

Another topic of concern has been reduced liquidity in times of crisis, making it extremely difficult to execute on wholesale rebalancing transactions for cash bond portfolios. The ETF market, however, held up extremely well during this volatile period which appeared to be characterized by indiscriminate selling. In the face of that, our ETF trades to rebalance the portfolio were executed in an effective manner.

One point of contention has been related to pricing transparency and what “true” market levels are for Fixed Income securities. Some ETFs have cleared at levels that were at varying discounts to the Net Asset Value ("NAV") of underlying components of the index backing a specific ETF. Many experienced participants in the industry, however, agree that Fixed Income ETF prices reflect true market clearing levels where portfolio trades can be executed. If the underlying NAVs reflect truly executable levels as opposed to the "discounted" levels for ETFs trading in the market, then market makers should be able to arbitrage this away to a large extent. Limited cash bond liquidity has hindered that activity. Since FolioBeyond’s strategy utilizes only ETFs, our performance numbers are much more consistent with executable market levels for specific bond sectors.

To conclude, while our model strategy has had varying US Treasury/Agency exposures over time, the allocations to this sector have on average tended to be lower due to the higher risk-adjusted yields offered by alternate sectors. Consequently, the underperformance in this type of rapidly declining interest rate environment is expected, especially given how US Treasuries and MBS have received external support by massive Fed purchases. The good news is that there are dislocations of historic proportions in the markets which are comparable or potentially greater than the 2008 Financial Crisis. FolioBeyond's Fixed Income algorithm is well positioned to take advantage of sector rotation opportunities, within the confines of model risk limits, to provide strong risk-adjusted returns in subsequent months and years.