FolioBeyond Fixed Income Commentary For May 2021

Performance Summary

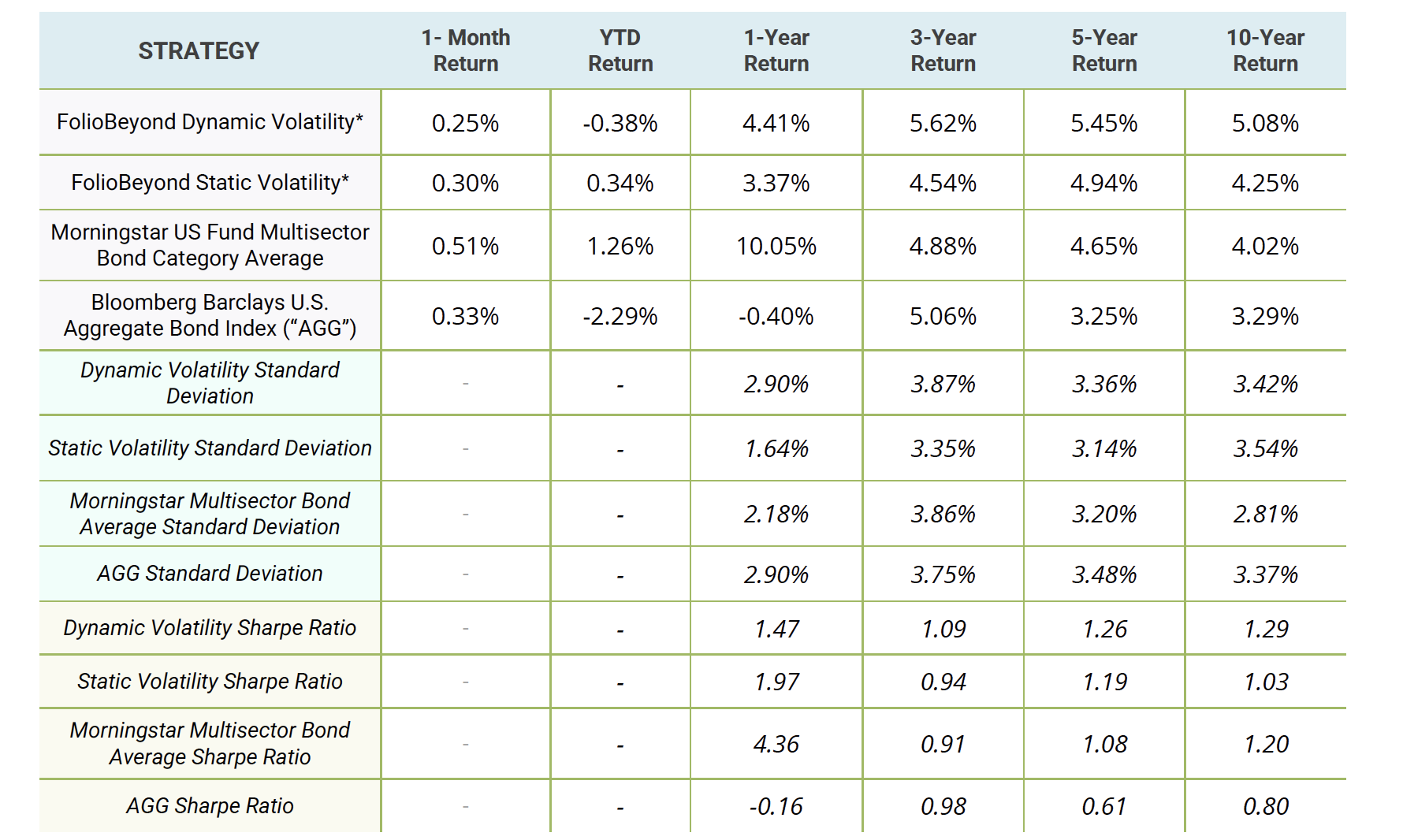

FolioBeyond's algorithmic Fixed Income strategy returned +0.25% and +0.30% in its dynamic and static volatility versions, respectively, in May. Year-to-date, the strategies have outperformed a comparable risk benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index ("AGG"), by 191 to 263 bps.

The bond market remained in a trading range with the 10-year Treasury yield oscillating in a 13-basis point range (1.56% - 1.69%). It ended the month 7 basis point lower than the previous month-end close. Our portfolios remained largely unchanged outside of a minor rebalancing, and positive returns were generated from current income and price gains.

Source: FolioBeyond’s returns are from SMAs on Interactive Brokers (from January 1, 2019 for Static Volatility and from November 3, 2020 for Dynamic Volatility) and back-tested simulated results prior to that. AGG and Multisector Bond Category returns are from Morningstar.

* FolioBeyond Dynamic and Static Volatility returns are net of underlying ETF fees and 30 bp assumed management fee. Although the information herein is believed to be reliable, FolioBeyond makes no representation or warranty as to its accuracy, and information and opinions reflected herein are subject to change at any time without notice. The past performance information presented herein is not a guarantee of future results.

Highlight: Update on Efficient Frontier

An integral part of FolioBeyond’s asset allocation model is the quantification of the risk/return tradeoffs available in the Fixed Income marketplace with the goal of targeting the efficient frontier subject to a desired risk target. A major aspect of this process is to update the risk/return attributes of the various subsectors of the Fixed Income market utilizing the latest available data.

The chart below plots out the individual risk/return attributes of the 23 subsectors of the Fixed Income market that we include in our portfolio optimization. At the lower end of the risk/return spectrum, we see the short duration sectors, along with higher credit exposures. As we move out to higher risk levels, we see the higher returning credit strategies, longer duration exposures and the levered mortgage REIT category at the upper right-hand corner.

The expected return calculations on the chart are based on forward looking yield estimates after pricing out embedded costs such as credit/default risk in corporate bonds and prepayment options in MBS and mortgage REITs. For inflation protected bonds, the consensus CPI forecast is incorporated into the return projection. On the risk side of the equation, historical risk analysis on passive ETFs is combined with adjustments made for current implied volatility levels reflected in the options market tied to rates. In summary, the scatter plot demonstrates the current risk/return tradeoffs available in the marketplace with the caveat of simply looking at individual sectors in isolation.

From a portfolio perspective, there are other relevant factors that come into play in optimizing the allocations. Correlation effects can provide positive benefits from combining uncorrelated assets that ultimately produce higher Sharpe ratios than if you had simply done a weighted average of the components. Additionally, single sector exposure limits, momentum effects and stress testing are incorporated.

The chart above also shows where FolioBeyond’s optimized portfolio sits relative to the efficient frontier curve. Our static volatility model targets the long-term volatility of AGG as represented by the green dot on the chart. Our dynamic volatility model tracks the trailing 1-year volatility of AGG and its risk/return target is represented by the blue dot. On a total return basis, FolioBeyond’s model is likely to produce meaningful sector rotation alpha from price gains to supplement current income as represented by the adjusted yield measure. Historically, 20-40% of total returns have been generated from capital gains.

A disciplined risk-controlled approach to Fixed Income portfolio management will lead to superior risk-adjusted returns in the long run, with less unexpected surprises along the way. FolioBeyond’s multi-factor model is designed to provide a comprehensive framework for rebalancing portfolios to desired risk targets. Our model portfolios are available on Folio Institutional and Boutique Exchange, and as a S-Network FolioBeyond Optimized Fixed Income Index on SMArtX and C8 Technologies. Please contact us to explore how our portfolio solutions can fit into your overall Fixed Income allocation.